By Wendy Cutler and Danny Russel

Editors Note: We are sending this week’s issue of Asia Policy Brief a day early to preview the upcoming high-stakes summit between U.S. President Donald Trump and Chinese President Xi Jinping. Wendy Cutler, Senior Vice President of the Asia Society Policy Institute (ASPI), and Danny Russel, Distinguished Fellow at ASPI, explain what’s on the agenda and what to expect. Keep an eye on your inbox: An issue of Asia ASAP will drop later this week with our experts’ rapid reactions to the summit.

(Photo by Andrew Harnik/Getty Images)

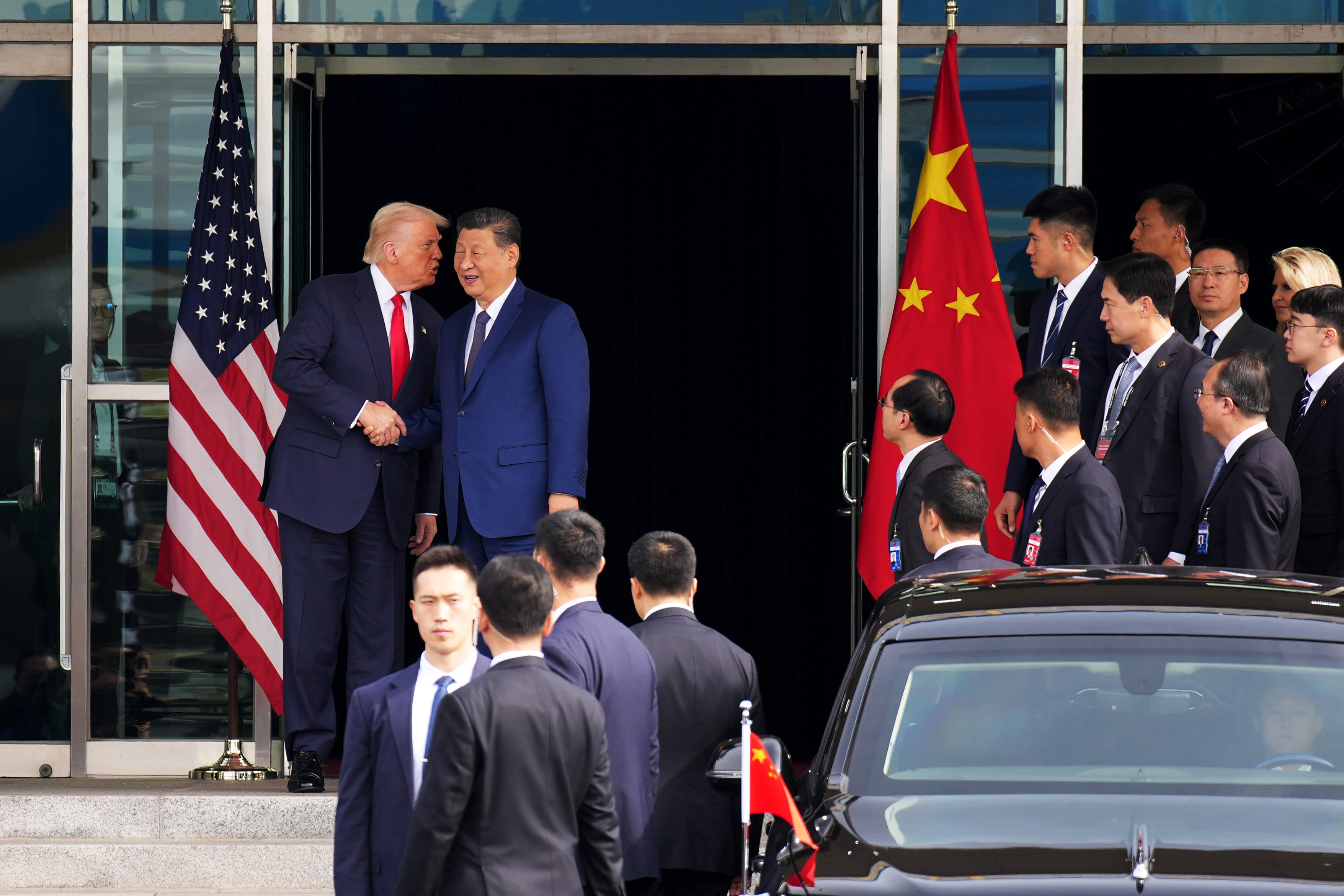

State of Affairs: Trump Goes to China

Presidents Trump and Xi are scheduled to meet Thursday and Friday in Beijing for their first face to face meeting since October’s summit in Busan. The leaders were originally set to convene in early April, but the U.S.-Israel-Iran conflict prompted Trump to delay his visit to China. President Trump hoped to arrive in Beijing inflated by victory in the Middle East, but the the conflict has instead exposed American vulnerabilities and reinforced Beijing’s concerns about energy security and maritime chokepoints. The war in the Middle East is now expected to be an important point of discussion, as will U.S. support of Taiwan, which Beijing is likely to push President Trump to dial back on.

Trade, investment, and related economic issues are also expected to be high on the agenda. After tit-for-tat tariff escalation in 2025, both leaders reached a trade truce when they met last October, bringing some welcome stabilization to the relationship. Largely due to high tariffs imposed by the U.S., its trade deficit with China fell by almost 32 percent last year, and further declines are expected this year. Nevertheless, tensions surrounding trade in strategic products, supply chain vulnerabilities, non-market economy policies and practices, excess manufacturing capacity, and broader economic security concerns continue, with both sides courting third counties to join their camp.

Why It Matters: Stabilization, Not Resolution

Both leaders seek stabilization, not resolution of the underlying strategic rivalry. Advanced technology, export controls, rare earths and critical minerals, AI risk management, strategic security, fentanyl precursor chemicals, and law enforcement cooperation are all candidates for discussion, but little groundwork has been laid on most of these matters for real results.

Trump comes to Beijing as a demandeur needing calm on his Pacific flank while heavily engaged in the Gulf. He may seek China’s diplomatic help with Teheran, particularly in opening the Strait of Hormuz, and limits on support flowing to Iran’s economy and military. Beijing, meanwhile, wants to protect shipping and energy imports, avoid further economic damage from higher energy prices and weakened export demand, and avoid direct confrontation with Washington.

We can also expect exchanges on North Korea, the South China Sea, and Chinese pressure on Japan, but few concrete outcomes. Taiwan is non-negotiable issue for Beijing, and Xi is likely to encourage Trump to continue delaying approval for a $14 billion arms sale package to Taiwan. Xi will try to reinforce Trump’s resistance to advice from China hawks in Washington and persuade him that Beijing’s outreach to Taiwan’s opposition shows “peaceful reunification” remains possible.

Beyond extending the nominal truce, likely outcomes are mostly pledges and process: resumed military communications, fentanyl measures, Gulf security consultations, working groups, promises to expand flights and people-to-people exchanges, and plans for additional summit meetings this year.

With respect to economic deliverables, expectations remain modest. We may see announcements by China to buy more American goods, including agriculture and aircraft, a relatively easy lift for Beijing. Prioritizing stabilization in the bilateral relationship, both sides may confirm and extend the October trade truce for another year or so. An announcement to establish a Board of Trade to “optimize” trade in non-sensitive sectors is on the docket, with the United States seeing this a venue to rebalance and more effectively manage trade. Finally, we may also see the establishment of a Board of Investment, but this concept seems to be more controversial in the U.S. and less developed.

Notably absent will be a push by Washington for much-needed structural reforms in China. Past efforts to spur such reforms have largely failed, leading the Administration to be more pragmatic and transactional and leaving to a later date seeking Chinese agreement to roll back its state-led policies and practices and increase domestic consumption, a laudable but fraught effort.

What to Watch

Trade: Of particular interest will be whether Beijing gains any traction on seeking further relaxation of U.S. export controls on advanced technologies, reduction in tariffs, or any assurances on outcomes from the two recently-launched U.S. Section 301 investigations on industrial excess capacity and forced labor. With the impressive group of American CEOs joining President Trump in Beijing, we may see some preliminary announcements of commercial deals, but given the last-minute invitations to join the summit, time may be insufficient to get these deals over the finish line. The mandate of the Board of Trade will be worth close scrutiny, particularly whether Beijing buys into a “managed trade” and “rebalancing“ approach, and which specific products would fall under its jurisdiction.

Taiwan: Trump’s language on Taiwan will be closely scrutinized during and after the visit. Given his tendency to echo leaders he admires, Beijing may hope he repeats Chinese formulations about “opposing Taiwan independence,” supporting “peaceful reunification,” or warning against “provocative actions” by Taiwan’s leader. Even subtle rhetorical shifts would advance China’s effort to demoralize and isolate Taiwan. Watch also for movement—in either direction—on the pending Taiwan arms package that Beijing strongly opposes.

Tehran: Another key question is how Beijing balances appearing helpful to Trump on Iran while maintaining its public opposition to military strikes and violations of sovereignty. Will China claim credit for encouraging Iranian flexibility in negotiations? Will it raise concerns and asks regarding economic fallout of the conflict? Watch carefully for signs that Trump offers practical accommodations in return, including privileged treatment for Hormuz transit, flexibility on Iranian oil purchases, or reduced scrutiny of Chinese shipping. Trump may claim Xi made firm commitments to curb dual-use exports to Iran, but whether Beijing corroborates that will matter.

Messaging and Future Meetings: As always, differences between the two sides’ readouts may prove more revealing than the official statements themselves. There may be further word on President Xi’s reciprocal visit to Washington this fall and/or participation in the APEC and G20 meetings, scheduled for Shenzhen and Florida, later this year. Following the visit, Trump’s comments or social media posts on North Korea or Japan may also offer clues about Xi’s private messaging, particularly if Trump begins echoing Chinese narratives about Japanese “remilitarization” or the need for talks with Pyongyang on Kim Jong Un’s terms.

Stay Up to Date with ASPI

Watch Kevin Rudd and Ian Bremmer discuss the U.S.-China relationship and wider geopolitical moment at Dr. Rudd’s first public event since returning to the Asia Society as Global President and CEO.

Watch Wendy Cutler in conversation with Stephen P. Vaughn, Ambassador Craig Allen, and Bob Davis about what lessons President Trump can take from the U.S.-Japan trade wars of the 1980s as he prepares to meet President Xi in Beijing.

Join us on Thursday, May 21 for an online panel discussion with Kevin Rudd, Wendy Cutler, Danny Russel, Orville Schell, Jing Qian, and Lizzi C. Lee on the outcomes of the Trump-Xi summit.

Register for a webinar to discuss what the Trump-Xi summit may reveal about the future of the Taiwan Strait on Tuesday, May 19, featuring Lyle Morris, David Sacks, Chung-min Tsai, and Yuqun Shao.